Value of a stock = EPS * PE

While EPS is the business fundamentals, PE is not just fundamentals but also a function of the cost of capital (which is a combination of risk-free rate and beta of the stock) Steadier the earnings lower the beta hence lower cost of capital and higher earnings

volatility means higher beta, implying higher cost of capital. When there is a cyclical recovery in earnings, beta for the cyclical earnings also comes down. You get earnings growth as well as higher valuations.

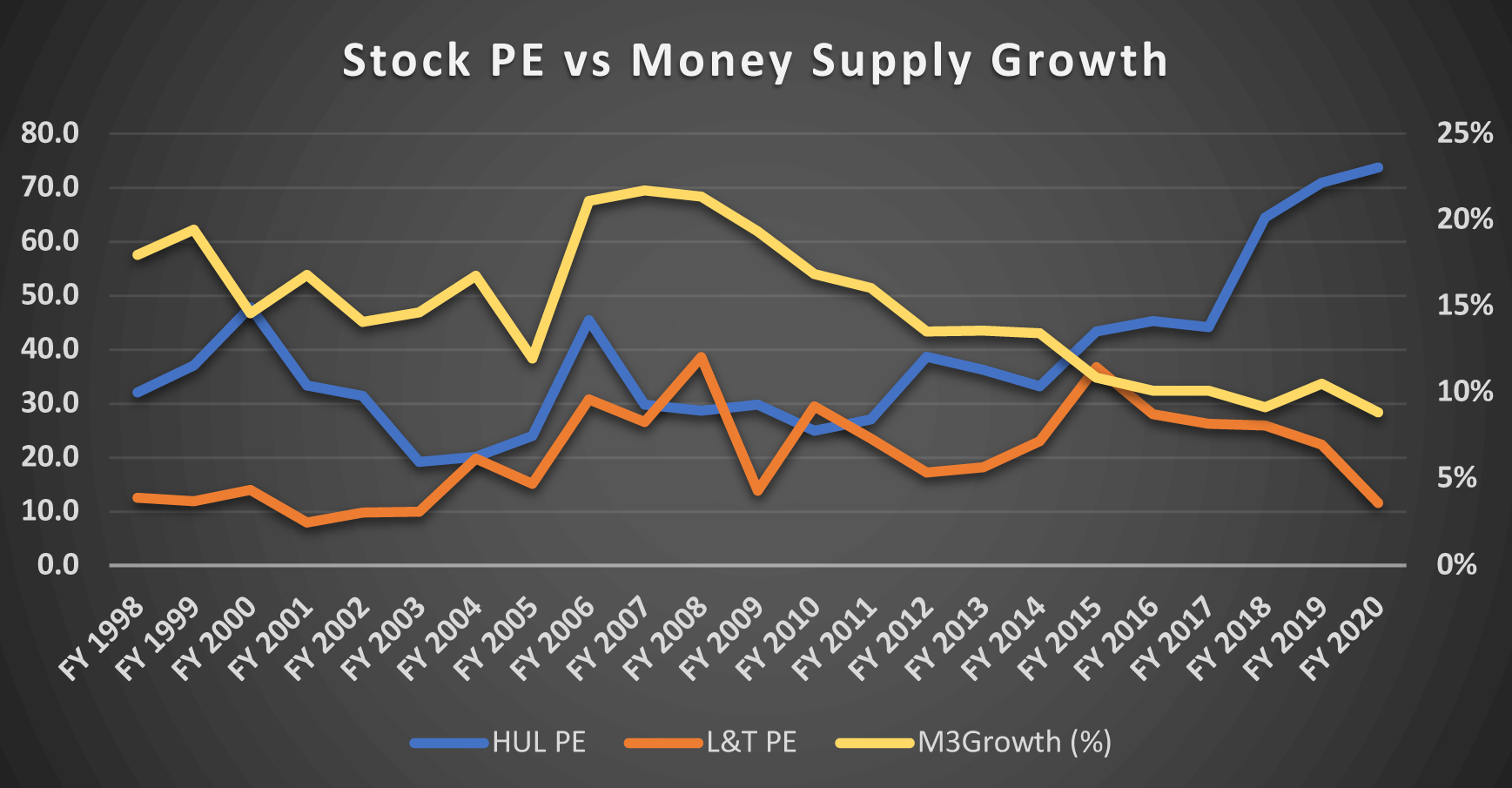

This re-rating/de-rating phenomenon is very well captured in the HUL and L&T PE chart below. In the last cycle 1998-2003 HUL peaked at 48x earnings. Recovery followed with a sharp earnings and PE recovery for L&T.

Post global financial crisis, Indian capex cycle has not recovered due to continued stress in the banking sector.

While earnings for HUL have been steady but the PE has expanded massively driven by lower cost of capital. L&T has been de-rated.

Post COVID banking sector stress will go up. For cyclical recovery credit growth needs to pick-up. Let’s keep an eye on banking sector; Infusion of capital, bad bank to clean up the NPL, structural reforms to get animal spirits back; for a turn in the cycle.

Till the cycle shows signs of revival, can the steady earners continue on the re-rating journey? Should cheap cyclicals be bought waiting for mean reversion? Globally technology stocks have been on fire, FANG in US and BAT in China. Can Reliance take that spot in India?